Production Function Estimation Methods and Total Factor Productivity Measurement — Industrial Policy Course

Author

Sinthavanh CHANTAVONG (TA); Christian Otchia (Instructor), GSID, Nagoya University

Published

November 5, 2025

Overview

This tutorial covers practical estimation of production functions and total factor productivity (TFP) using Stata. We implement four core estimation methods: OLS, Fixed Effects (FE), Olley-Pakes (OP), and Levinsohn-Petrin (LP). These methods represent increasing levels of sophistication in addressing econometric challenges inherent in production function estimation.

Theory: Production Functions and TFP

The Cobb-Douglas Production Function

The standard production function relates output to inputs:

TFP (\(A_{it}\) or \(\omega_{it}\)) represents output not explained by measured inputs. It captures: - Technological improvements - Management quality - Organizational efficiency - Unobserved capital (R&D, human capital, reputation) - Measurement errors in inputs/outputs

Estimation: Once we estimate elasticities (\(\hat{\beta}_k, \hat{\beta}_l, \hat{\beta}_m\)), we calculate TFP residuals:

The hands-on portion of this tutorial focuses on four core methods only:

OLS - Ordinary Least Squares (baseline)

FE - Fixed Effects (controls for firm heterogeneity)

OP - Olley-Pakes (proxy method using investment)

LP - Levinsohn-Petrin (proxy method using materials)

The following advanced estimators have been omitted from the step-by-step code to keep the notebook focused:

Ackerberg-Caves-Frazer (ACF)

Wooldridge (dynamic GMM)

Robinson (semi-parametric)

These methods remain important for research-level work. They are omitted here because they require additional conceptual material (instrument timing, nonparametric bandwidth selection, or dynamic-GMM technicalities) that would lengthen the practical exercise. See the References and the prodest documentation for worked examples and further reading.

Now productivity is observable (function of observables), so OLS works!

Step 3: Estimate Parameters

Use nonparametric or semi-parametric methods to estimate \(h(\cdot)\) and \(\beta\) coefficients simultaneously.

How This Solves Problem 1: Simultaneity Bias

The Problem: Labor and materials are chosen after observing \(\omega_{it}\), creating \(\mathbb{E}[\omega_{it} | L_{it}, M_{it}] \neq 0\)

The Solution: - Proxy variables (investment or materials) respond to \(\omega_{it}\) in a predictable way (monotonically increasing) - By inverting this relationship, we recover \(\omega_{it}\) - Now we can control for it, removing the correlation

Result: Simultaneity bias eliminated ✅

How effectively? - ✅ Very effective IF proxy is truly monotonically increasing in productivity - ⚠️ May be weak if firms have other reasons to choose proxy (financial constraints, adjustment costs)

How This Solves Problem 2: Omitted Variable Bias

The Problem: Time-invariant productivity differences \(\omega_i\) correlate with input choices, biasing coefficients

The Solution (depends on method):

Olley-Pakes & Levinsohn-Petrin (OP, LP): - Explicitly model firm exit decision as function of \(\omega_{it}\) and capital

- Use this to correct for selection bias in sample - Accounts for firms exiting based on productivity realizations Result: Omitted variable bias substantially reduced ✅

How effectively? - ✅ Effective at controlling permanent firm differences - ⚠️ Cannot address time-varying unobserved heterogeneity (e.g., new technology adoption, sudden management change)

Scope note — methods excluded from this tutorial

To keep the practical tutorial focused and concise, we limit hands-on estimation to four core methods: OLS, Fixed Effects (FE), Levinsohn-Petrin (LP), and Olley-Pakes (OP). The following advanced estimators are intentionally omitted from the practical steps below: ACF (Ackerberg-Caves-Frazer), Wooldridge (dynamic GMM), and Robinson (semiparametric).

Why omitted: these methods are valuable but add complexity (different assumptions, instrument timing, or nonparametric bandwidth selection) that distracts from the core learning goals. If you need them for research, see the references (Van Beveren 2010; Ackerberg et al. 2015; Wooldridge 2009; Robinson 1988) and the prodest documentation.

Key Takeaways (revised):

OLS fails for simultaneity and selection — use only as a baseline

Fixed Effects controls time-invariant heterogeneity but not simultaneity

Proxy methods (OP, LP) recover productivity via a control function and address simultaneity and selection when their assumptions hold

Trade-offs: OP can drop zero-investment firms; LP is usually preferred in applied work due to better sample coverage

PART II: PRACTICAL ESTIMATION

Code Execution Instructions

This tutorial contains Stata code examples that you should run in your own Stata environment. The code blocks below are for reference and copying. To execute them:

Install Required Packages: Run ssc install prodest in Stata

Copy and Run: Copy each code block into your Stata do-file editor

Execute Step-by-Step: Run the commands in the order shown

Compare Results: Note how coefficients change across methods

Expected Runtime: Each estimation method takes 1-5 minutes depending on your computer.

Step 1: Load the Data

IMPORTANT: Start by installing the prodest package and loading the Chilean manufacturing dataset from GitHub. Run this code in Stata:

Show the code

// SETUP: Install prodest package and check versionssc install prodest, replace// REPRODUCIBILITY: Check Stata version and prodest versiondisplay"Stata Version: " c(stata_version)which prodest

Running C:\Users\sinth\ado\personal\profile.do ...

command window is unrecognized

r(199);

checking prodest consistency and verifying not already installed...

all files already exist and are up to date.

Stata Version: 18

C:\Users\sinth\ado\plus\p\prodest.ado

*! version 1.0.1 15Sep2016

*! version 1.0.2 22Sep2016

*! version 1.0.3 30Sep2016 Fixed a major bug, add first stage residuals options

> , seeds option, evaluator option and postestimation

*! version 1.0.4 10Feb2017 Fixed a major bugs in winitial() matrix in MrEst, fi

> xed minor bug on Wrdg control and names,

*! added translog production fu

> nction, added starting points option for estimation, add check for multiple s

> tate and proxy

*! version 1.0.5 06Jun2017 Fixed minor bugs in control variable management, err

> or management of translog production function, added a new feature

*! in table reporting (prod fun

> ction CB / Tranlsog), fixed major bugs in predict

*! version 1.1.1 13Feb2018 SJ review: Fixed an issue with var names that preven

> ted more than 10 state variable to be used at once, added the "Robinson/ACF"

> model,

*! added

> the "gmm" option for Wrdg models, fixed the linear version of Wrdg model

*! version 1.1.2 14Mar2018 Added the eret loc FSres in case of first stage resi

> duals, in order to ensure that predict, omega can be launched

*! version 1.2.1 26Jun2018 Made several minor fixes on helpfile and dofile sugg

> ested by Sven-Kristjan Bormann. Added his dialog box file to the package

*! version 1.2.2 30Jul2018 Added the controls to the Wooldridge - plain - metho

> d.

*! authors Gabriele Rovigatti, Bank of Italy, Rome, Italy. mailto: gabriele.rov

> igatti@gmail.com | gabriele.rovigatti@esterni.bancaditalia.it

*! Vincenzo Mollisi, Bolzano University, Bolzano, Italy & Tor Vergata U

> niversity, Rome, Italy. mailto: vincenzo.mollisi@gmail.com

Then load the data:

Show the code

// Load the Chilean manufacturing dataset from the prodest GitHub repository:clearall// clear all objects from memory// Load data from GitHub repositoryinsheetusing"https://raw.githubusercontent.com/GabrieleRovigatti/prodest/master/stata/data/prodest.csv", names clear// Check data structuredisplay"Data loaded: " _N " observations"describesummarize

(8 vars, 2,544 obs)

Data loaded: 2544 observations

Contains data

Observations: 2,544

Variables: 8

-------------------------------------------------------------------------------

Variable Storage Display Value

name type format label Variable label

-------------------------------------------------------------------------------

id long %12.0g

year int %8.0g

log_y float %9.0g

log_k float %9.0g

log_lab1 float %9.0g

log_lab2 float %9.0g

log_materials float %9.0g

log_investment float %9.0g

-------------------------------------------------------------------------------

Sorted by:

Note: Dataset has changed since last saved.

Variable | Obs Mean Std. dev. Min Max

-------------+---------------------------------------------------------

id | 2,544 15770.49 7355.94 10007 40475

year | 2,544 2001.042 3.223341 1996 2006

log_y | 2,544 13.00315 1.462817 8.769663 18.57996

log_k | 2,544 11.6683 2.156707 2.70805 18.21685

log_lab1 | 2,544 1.769697 1.357786 0 6.861712

-------------+---------------------------------------------------------

log_lab2 | 2,544 1.679659 1.447586 0 6.439351

log_materi~s | 2,544 4.108881 1.546106 0 9.944486

log_invest~t | 2,544 11.13678 2.33267 1.072183 18.08836

Dataset Information

401 unique firms

2,544 firm-year observations

Period: 1996-2006 (9-year panel, unbalanced)

Industry: Chilean manufacturing

Source: Levinsohn & Petrin (2003), data repository for prodest package

Variables Pre-Logged: All log_* variables are pre-logged in the dataset (no log transformation needed)

Step 2: Data Overview

Variable

Description

Type

log_y

Log of output (value added)

Dependent variable

log_k

Log of capital stock

State variable (quasi-fixed)

log_lab1

Log of white-collar labor

Free variable (flexible)

log_lab2

Log of blue-collar labor

Free variable (flexible)

log_materials

Log of materials expenditure

Proxy variable (for LP)

log_investment

Log of investment

Proxy variable (for OP)

id

Firm identifier

Panel ID

year

Time period (1995-2003)

Panel time variable

Step 3: Panel Configuration

Show the code

// Set panel structure (already loaded from GitHub)setmoreoffxtset id yearxtsum// Panel descriptionxtdescribe

Panel variable: id (unbalanced)

Time variable: year, 1996 to 2006, but with gaps

Delta: 1 unit

Variable | Mean Std. dev. Min Max | Observations

-----------------+--------------------------------------------+----------------

id overall | 15770.49 7355.94 10007 40475 | N = 2544

between | 7373.884 10007 40475 | n = 497

within | 0 15770.49 15770.49 | T-bar = 5.11871

| |

year overall | 2001.042 3.223341 1996 2006 | N = 2544

between | 2.818345 1996 2006 | n = 497

within | 2.509037 1994.375 2007.842 | T-bar = 5.11871

| |

log_y overall | 13.00315 1.462817 8.769663 18.57996 | N = 2544

between | 1.458466 9.346007 18.08074 | n = 497

within | .2722173 10.78107 14.88404 | T-bar = 5.11871

| |

log_k overall | 11.6683 2.156707 2.70805 18.21685 | N = 2544

between | 1.993314 4.261184 17.83619 | n = 497

within | .7463301 4.769393 18.01236 | T-bar = 5.11871

| |

log_lab1 overall | 1.769697 1.357786 0 6.861712 | N = 2544

between | 1.198308 0 5.851838 | n = 497

within | .6443298 -2.376207 5.093458 | T-bar = 5.11871

| |

log_lab2 overall | 1.679659 1.447586 0 6.439351 | N = 2544

between | 1.265404 0 6.098074 | n = 497

within | .7979751 -2.521169 5.600971 | T-bar = 5.11871

| |

log_ma~s overall | 4.108881 1.546106 0 9.944486 | N = 2544

between | 1.50085 .5776227 9.304231 | n = 497

within | .5237046 -.9002941 6.303847 | T-bar = 5.11871

| |

log_in~t overall | 11.13678 2.33267 1.072183 18.08836 | N = 2544

between | 2.132428 3.084425 17.54119 | n = 497

within | .9065335 3.457233 18.41997 | T-bar = 5.11871

id: 10007, 10016, ..., 40475 n = 497

year: 1996, 1997, ..., 2006 T = 11

Delta(year) = 1 unit

Span(year) = 11 periods

(id*year uniquely identifies each observation)

Distribution of T_i: min 5% 25% 50% 75% 95% max

1 1 2 4 9 11 11

Freq. Percent Cum. | Pattern

---------------------------+-------------

56 11.27 11.27 | 11111111111

29 5.84 17.10 | ........111

29 5.84 22.94 | .......1111

24 4.83 27.77 | 1..........

19 3.82 31.59 | 111111111..

18 3.62 35.21 | .........11

16 3.22 38.43 | ..........1

16 3.22 41.65 | 111111.....

12 2.41 44.06 | ....1......

278 55.94 100.00 | (other patterns)

---------------------------+-------------

497 100.00 | XXXXXXXXXXX

⚠️ CRITICAL: Understanding TFP Prediction in Proxy Methods

Before running estimations, understand the difference between omega and residuals:

Returns: Best available estimate of \(\omega_{it}\) given the method

Example: Do NOT Mix Methods

// ❌ ERROR: This will fail - Wooldridge doesn't support fsresidualsprodest log_y, ... met(wrdg) fsresiduals(fs_wrdg)predict tfp, omega // ERROR: "omega option only works with fsresiduals"// ✅ CORRECT: Use residuals for Wooldridgeprodest log_y, ... met(wrdg)predict tfp, residuals // Works: returns TFP estimate

Step 4: Method 1 - OLS Regression

Getting Started: OLS as a Baseline

Beginning with OLS estimation provides a baseline reference. This approach serves as the starting point for understanding how alternative methods modify estimates. Run this code:

Baseline for Comparison: Subsequent methods will show how alternative approaches modify these baseline estimates

Illustrative Result: In the Chilean manufacturing data example, OLS yields: - Capital elasticity: 0.321 - White-collar labor: 0.458

- Blue-collar labor: 0.365

The relatively large labor coefficients might warrant further investigation using alternative approaches that address endogeneity concerns.

\(\omega_{it}\) = True productivity (persistent, what we want)

\(\varepsilon_{it}\) = Random noise (measurement error, transitory shocks)

Why This Matters

Because inputs (L, M) are correlated with \(\omega_{it}\), OLS coefficients are biased: - Labor coefficients: UPWARD biased (firms hire more when productive) - Capital coefficient: DOWNWARD biased (slow adjustment, selection effects)

Step 5: Method 2 - Fixed Effects

Fixed Effects (FE) Approach

Fixed effects estimation removes firm-specific time-invariant heterogeneity through within-firm transformation:

Selection Issues: Firm exit decisions that vary with current productivity

Time-Varying Heterogeneity: Factors that change over time and remain unobserved

Comparison with OLS: In the Chilean manufacturing example, FE yields considerably smaller coefficients (capital: 0.069, labor: 0.084–0.078) compared to OLS (0.321, 0.458, 0.365). This difference suggests that OLS estimates may partially reflect time-invariant firm differences rather than input elasticities alone.

Price Deflation Issue (When Using Deflated Sales)

If using deflated sales instead of quantities, note that firm-level price deviations from industry-level deflators introduce omitted price bias. Fixed effects cannot address this. Best practice: Use quantity-based output when available, or use industry-wide comparisons (Van Beveren, 2010).

Step 6: Advanced Methods Overview

Proxy Variable Approaches

The remaining methods (OP, LP) use proxy variables to control for unobserved productivity.

The key insight:

Investment or materials expenditure reveals information about productivity

By inverting these relationships, we can recover\(\omega_{it}\) and use it to correct simultaneity bias.

Step 7: Method 3 - Olley-Pakes (OP)

Key Idea

Use investment as a proxy for unobserved productivity.

Assumptions: - Investment is monotonically increasing in productivity (more productive firms invest more): \(\frac{\partial I_{it}}{\partial \omega_{it}} > 0\) - Investment is observed without measurement error - Requires at least \(T \geq 2\) time periods

Important Caveat: Observations with zero investment (\(I_{it} = 0\)) are typically dropped during estimation because the invertibility assumption breaks down. This can cause substantial sample loss.

Show the code

// Check for zero investment observations BEFORE running OPcountif log_investment == .countif log_investment < -10 // Very small investment = near-zero// Olley-Pakes estimationprodest log_y, free(log_lab1 log_lab2) state(log_k) proxy(log_investment) /// va met(op) poly(4) reps(40) id(id) t(year) fsresiduals(fs_op)estimatesstore op_est// Display OP results and sample sizeestimatestable op_est, b(%7.4f) se(%7.4f) stats(N)display"WARNING: Compare N above to full sample size 2544"// Extract TFPpredict op_tfp, omega // CRITICAL: Use omega for actual TFP in proxy methodslabelvariable op_tfp "TFP: Olley-Pakes (investment proxy)"

0

0

.........10.........20.........30.........40

op productivity estimator Cobb-Douglas PF

Dependent variable: value added Number of obs = 2544

Group variable (id): id Number of groups = 497

Time variable (t): year

Obs per group: min = 1

avg = 5.1

max = 11

------------------------------------------------------------------------------

log_y | Coefficient Std. err. z P>|z| [95% conf. interval]

-------------+----------------------------------------------------------------

log_lab1 | .313561 .0304823 10.29 0.000 .2538168 .3733053

log_lab2 | .2495986 .0233405 10.69 0.000 .203852 .2953452

log_k | .1558824 .0720795 2.16 0.031 .0146091 .2971556

------------------------------------------------------------------------------

Wald test on Constant returns to scale: Chi2 = 11.44

p = (0.00)

------------------------

Variable | op_est

-------------+----------

log_lab1 | 0.3136

| 0.0305

log_lab2 | 0.2496

| 0.0233

log_k | 0.1559

| 0.0721

-------------+----------

N | 2544

------------------------

Legend: b/se

WARNING: Compare N above to full sample size 2544

Computational Time: Approximately 1–3 minutes (varies with number of replications and polynomial order)

OP: Approach Overview

The Olley-Pakes method uses investment as a proxy variable. The approach assumes that investment decisions reflect firm productivity levels:

Key Considerations

Sample Coverage: Observations with zero investment may be excluded, potentially reducing effective sample size by 10–30%

Data Requirements: Requires at least 3 time periods

Labor Treatment: Treats labor as exogenous conditional on capital and investment

Single-Product Assumption: If firms produce multiple products, TFP estimates may reflect product-mix effects (Van Beveren, 2010; Bernard et al., 2005). Consider restricting to single-product firms for robustness.

Illustrative Results

In the Chilean manufacturing example, OP yields: - Capital elasticity: 0.156 - White-collar labor: 0.314 - Blue-collar labor: 0.250

These compare to FE (0.069, 0.084, 0.078) and OLS (0.321, 0.458, 0.365).

Step 8: Method 4 - Levinsohn-Petrin (LP)

LP Approach

Use materials expenditure as the proxy variable:

Practical Considerations: - Materials input is typically available across firms and time periods - Fewer missing observations than investment-based approaches - Moderate computational requirements - Commonly used baseline approach in practice

Show the code

// Levinsohn-Petrin estimationprodest log_y, free(log_lab1 log_lab2) state(log_k) proxy(log_materials) va met(lp) opt(dfp) reps(50) id(id) t(year) fsresiduals(fs_lp)estimatesstore lp_est// Display LP results//estimates table lp_est, b(%7.4f) se(%7.4f) stats(N)// Extract TFPpredict lp_tfp, omega // CRITICAL: Use omega for actual TFP in proxy methodslabelvariable lp_tfp "TFP: Levinsohn-Petrin (materials proxy)"

.........10.........20.........30.........40.........50

lp productivity estimator Cobb-Douglas PF

Dependent variable: value added Number of obs = 2544

Group variable (id): id Number of groups = 497

Time variable (t): year

Obs per group: min = 1

avg = 5.1

max = 11

------------------------------------------------------------------------------

log_y | Coefficient Std. err. z P>|z| [95% conf. interval]

-------------+----------------------------------------------------------------

log_lab1 | .2011151 .0289476 6.95 0.000 .1443789 .2578514

log_lab2 | .1696221 .0237969 7.13 0.000 .1229811 .2162632

log_k | .1200285 .0380805 3.15 0.002 .0453922 .1946649

------------------------------------------------------------------------------

Wald test on Constant returns to scale: Chi2 = 71.68

p = (0.00)

Computational Time: Approximately 1–2 minutes (faster than OP due to better material coverage)

What LP May Address

✅ Simultaneity: Materials proxy controls for productivity when estimating labor coefficients

✅ Selection: Models exit probability explicitly

✅ Sample Coverage: Typically retains more observations than OP since materials are available for most firms

What LP May Address

✅ Simultaneity: Materials proxy controls for productivity when estimating labor coefficients

✅ Selection: Models exit probability explicitly

✅ Sample Coverage: Typically retains more observations than OP since materials are available for most firms

Example Results

In Chilean manufacturing data, LP produces: - Capital elasticity: 0.120 (suggests moderate capital importance) - White-collar labor: 0.201 (lower than OLS, suggesting some endogeneity) - Blue-collar labor: 0.170 (suggests modest labor response to productivity)

These results represent a middle ground between Fixed Effects estimates (which may underestimate due to simultaneity bias) and OLS estimates (which may overestimate due to omitted variable bias).

Step 9: Robustness Checks and Validation

Returns-to-Scale Test (RTS)

For all methods, test if \(\text{RTS} = \beta_k + \beta_{l1} + \beta_{l2} = 1\) (constant returns):

Show the code

// Test RTS = 1 for each method (example with LP)estimatesrestore lp_estnlcom rts: (_b[log_k] + _b[log_lab1] + _b[log_lab2])// Interpret:// RTS ≈ 1.0: Constant returns (competitive markets, efficient scale)// RTS > 1.0: Increasing returns (learning, fixed costs, returns to specialization)// RTS < 1.0: Decreasing returns (managerial constraints, congestion)

Key Notes: - ⭐ = Always use predict ..., omega for proxy methods (not residuals) - Sample size loss due to time period requirements: Wooldridge loses ~10-20% due to \(T \geq 3\) - All proxy methods require 2+ time periods, NOT 3+ (except Wooldridge)

Expected Patterns

Coefficient Patterns

Based on Van Beveren (2010) and our results from Chilean manufacturing data:

Capital Coefficients: FE < LP < OP < OLS

- OLS is downward BIASED by selection (high-productivity firms use more capital) - Proxy methods (OP/LP) correct for simultaneity but FE captures only within-firm variation - Ranking: OLS > OP > LP > FE shows the correction for endogeneity

Labor Coefficients: FE < LP < OP < OLS

- OLS is UPWARD biased (firms hire more when productive) - Proxy methods reduce labor coefficients substantially - ACF refines LP further for even more conservative labor estimates

Interpreting Our Results

In our Chilean data: - Capital elasticity ranges from 0.069 (FE) to 0.321 (OLS) - FE only captures short-term adjustment (plants are quasi-fixed) - Proxy methods show intermediate estimates - Labor elasticity ranges from 0.084 (FE) to 0.458 (OLS) - Large OLS bias reflects simultaneity: productive firms hire more - Correcting for endogeneity cuts labor elasticity roughly in half

Interpretation: - \(\rho \approx 0.7\)-\(0.9\): High persistence (typical for manufacturing) - \(\rho < 0.5\): Productivity appears transitory (check for measurement error) - \(\rho \approx 1.0\): Non-stationary (problematic; suggests specification issues)

Scatter Plots: TFP Comparisons

Show the code

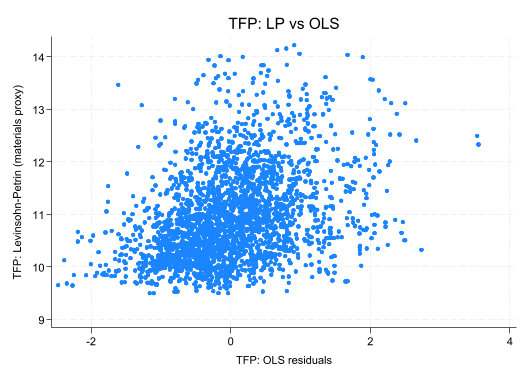

// Visual face validity checktwowayscatter lp_tfp ols_tfp, title("TFP: LP vs OLS") graphregion(style(none))

Show the code

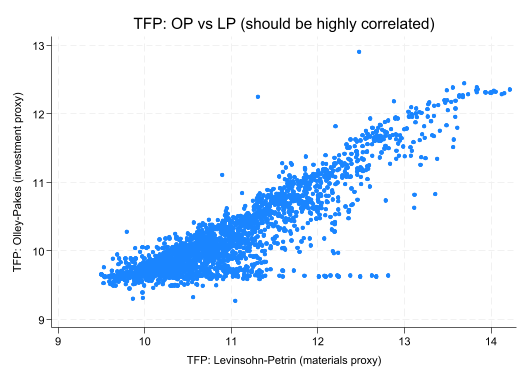

twowayscatter op_tfp lp_tfp, title("TFP: OP vs LP (should be highly correlated)")

Show the code

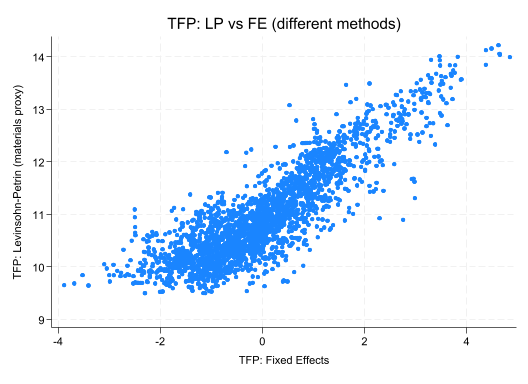

twowayscatter lp_tfp fe_tfp, title("TFP: LP vs FE (different methods)")

Show the code

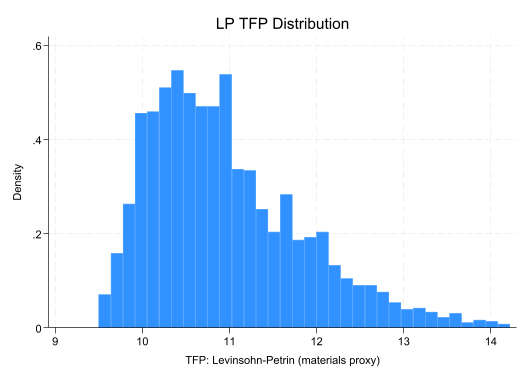

// Distribution checkhistogram lp_tfp, title("LP TFP Distribution")

(bin=34, start=9.4998198, width=.13879296)

Show the code

histogram op_tfp, title("OP TFP Distribution")

(bin=34, start=9.2711468, width=.10681677)

Face Validity Checks: - Are correlations high between similar methods (LP, OP)? - Do outliers make sense (unusual firms, measurement errors)? - Are distributions roughly normal (or log-normal)?

Quick Reference: Standard Commands

Data Loading & Setup

// Load data from GitHub

insheet using "https://raw.githubusercontent.com/GabrieleRovigatti/prodest/master/stata/data/prodest.csv", names clear

// Set panel structure

xtset id year

Method 1: OLS (Baseline)

How it works: Standard regression - assumes all inputs are exogenous

Problem Solving: - ❌ Simultaneity Bias: NOT solved - Labor/materials chosen after observing \(\omega_{it}\) - ❌ Omitted Variable Bias: NOT solved - Permanent firm differences uncontrolled

Expected Result: Reduced coefficients (especially capital). In Chilean data: \(\beta_K \approx 0.069\) (too low due to remaining simultaneity for free variables)

Note

Why FE alone isn’t enough: Fixed effects removes the permanent productivity difference, BUT labor is still chosen contemporaneously with \(\omega_{it}\). Within-firm time variation in productivity still correlates with labor choices.

Control Function:\[\omega_{it} = \phi_t(K_{it}, I_{it})\] where \(\phi_t\) is estimated nonparametrically (polynomial approximation)

Problem Solving: - ✅ Simultaneity Bias: SOLVED - Investment monotonically reveals \(\omega_{it}\), so control function eliminates correlation

- ✅ Omitted Variable Bias: SOLVED - Accounts for firm exit decisions using parametric exit model

Trade-off: - ⚠️ Zero Investment Problem: Observations with zero/very low investment must be dropped (~10-30% of sample) - ⚠️ Collinearity: Labor and productivity may be too collinear in first stage (addressed by ACF)

Control Function:\[\omega_{it} = \phi_t(K_{it}, L_{it}, M_{it})\]

Problem Solving: - ✅ Simultaneity Bias: SOLVED - Materials proxy reveals \(\omega_{it}\) through firm’s optimization

- ✅ Omitted Variable Bias: SOLVED - Jointly accounts for firm exit and permanent productivity differences

Advantages over OP: - ✅ Better sample coverage - Materials available for 95%+ of firms vs. investment for 60-70% - ✅ More stable estimates - No collinearity problem like OP - ✅ Faster computation - Fewer missing values to handle

Note: LP method supports fsresiduals() option, enabling predict ..., omega for TFP extraction. RECOMMENDED for practical applications.

prodest log_y, free(log_lab1 log_lab2) state(log_k) proxy(log_materials) /// va met(lp) opt(dfp) reps(50) id(id) t(year) fsresiduals(fs_lp)estimatesstore lp_estestimatestable lp_est, b(%7.4f) se(%7.4f) stats(N)predict lp_tfp, omega // CRITICAL: Use omega to get actual TFP, not residuals

Method Summary

The four core methods address different econometric challenges:

Method

Addresses

Limitation

Use When

OLS

None (baseline)

Simultaneity + selection bias

First pass only

FE

Time-invariant heterogeneity

Doesn’t fix simultaneity/selection

Firm-specific effects suspected

OP

Simultaneity + selection

Drops zero investment observations

Investment monotonic & observable

LP

Simultaneity + selection

Requires materials data

Materials widely available

Practical Recommendation: Estimate all four methods and compare results. Consistency across LP and OP provides stronger evidence than any single method.

Robustness Checks and Validation

After estimating all methods, verify your results with these checks:

Examine results for plausibility given theoretical priors

Consider comparison across multiple methods

For Your Coursework

Suggested Starting Point: 1. Run OLS and FE (baseline approaches) 2. Run at least one proxy method (LP is commonly used) 3. Compare coefficients across methods 4. Compute correlations between TFP estimates across methods 5. Test returns-to-scale hypothesis for each method 6. Discuss which concerns seem empirically relevant for your data

Possible Extensions: - Run additional proxy methods (OP, ACF, Wooldridge, Robinson) for comparison - Test sensitivity to specification choices (polynomial order, instrument set) - Analyze TFP persistence using lagged regression approaches - Examine graphical comparisons between TFP estimates - Relate TFP variations to observable firm characteristics

References

Survey and Implementation:

Van Beveren, I. (2012). Total Factor Productivity Estimation: A Practical Review. Journal of Economic Surveys, 26(1), 98-128.

Rovigatti, G., & Mollisi, V. (2018). Theory and Practice of Total-Factor Productivity Estimation: The Control Function Approach Using Stata. Stata Journal, 18(3), 618-662.

End of Tutorial

Your Assignment Tasks

Run all 4 core methods (OLS, FE, LP, OP) in Stata using the code provided above

Compare coefficients across methods (use estimates table command)

Analyze TFP correlations between methods

Write a report explaining:

Which biases each method addresses

How your coefficient estimates change

Which method you recommend for your data

Why TFP estimates differ across methods

Submit: Your Stata log file + coefficient comparison table + 2-page analysis

For questions or feedback, contact the course TA.

Course: Industrial Policy Institution: GSID, Nagoya University Last Updated: November 2025